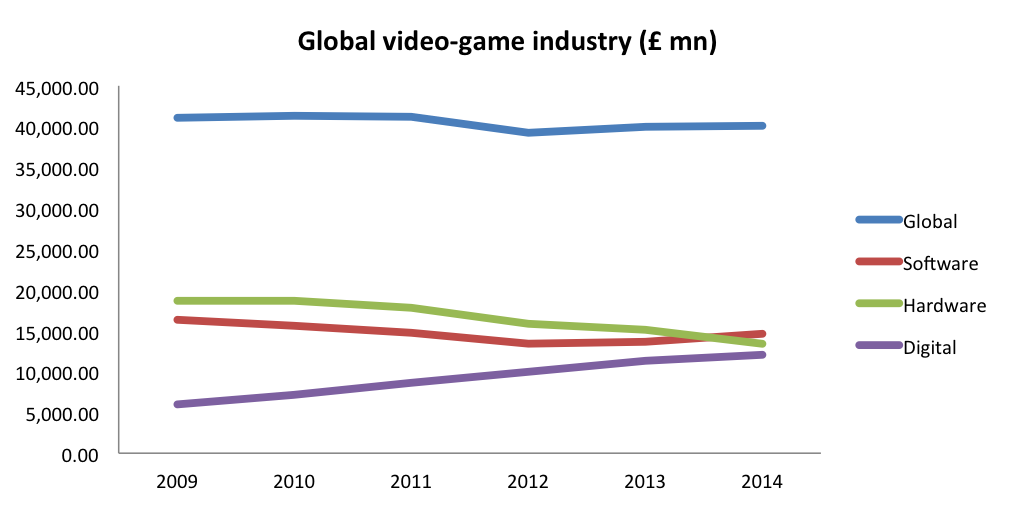

The news regarding the recent recovery of the global video-game market has been hailed as very positive; and it should be. The global market of video games exceeded £41bn in 2014, experiencing a growth rate of 6%. Although a positive development, the effects are not uniformly distributed among the industrial population. The question? How can we explore the effect of market change for different types of companies?

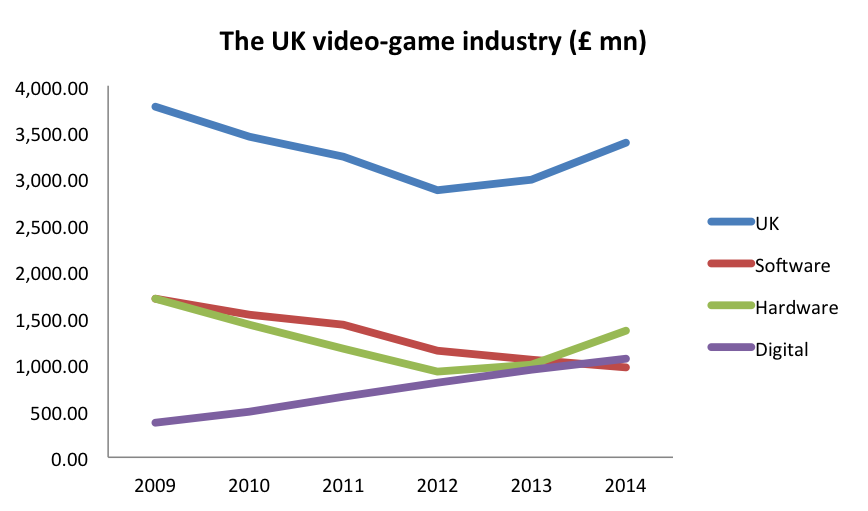

Before answering this question, let’s shift our view towards the UK video-game market. The national market reacted much too dramatically between 2009 and 2014. However, the market positively rebounded after 2014. The market grew by 11% (Euromonitor Passport 2015). Another impressive feat of the industry is that for the first time digital distribution exceeded the physical one in value. That can be safely attributed to the rapid growth of the mobile games market, which is one of the most dynamic market segments. However, the good news is not reflected on the population trajectory.

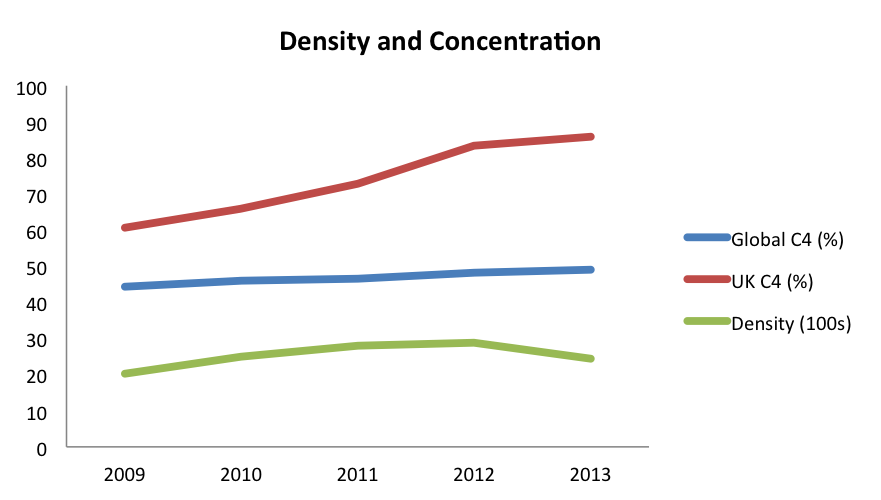

Density is the physical number of companies within an industry. Our sample consists of 1920 companies classified as “Ready-made interactive leisure and entertainment software development” (62011) and “Publishing of Computer games” (58210). The number of company may underestimate the actual population, and density, but it is big enough to allow us some safe, and useful, insights.

A potential answer to the population decrease during 2014 can be potentially related to the concentration of the market. Concentration is the fraction of the market that is controlled by the 4 biggest companies of the industry. During the last 6 years, concentration within the UK skyrocketed to 80% (global average is 49.1%). Small and medium sized companies in the UK were affected more adversely than the big companies, who were more capable of competing in the global market and thus increasing the concentration.

We delved further into the effects of density and concentration of the market to the survivability of developers and publishers within the UK. The company’s type is significant in predicting exit rates from the industry. Publishers’ survivability is lower compared to that of developers’ when concentration of the market increases. Through resource partitioning theory, we are able to interpret this phenomenon.

Arguably, publishers are acting as “generalists” within the industry, competing for resources that become more and more scarce (smaller market, bigger concentration). On the other hand, developers, locate and occupy small niche bubbles within the industry’s resource space. A lesson for entrepreneurs that aim to enter the industry would be to try and locate a particular market segment within the industry, and serve a niche customer segment. If they aim to adopt a “generalists” strategy, such as publishers, in a highly concentrated market, that would bring them against the industry’s big players threatening their survivability directly.

- Log in to post comments